Q1 Houzz Renovation Barometer Shows Mixed Expectations

January 16, 2019

Houzz Inc., a platform for home remodeling and design, has released the Q1 2019 Houzz Renovation Barometer, which tracks residential renovation market expectations, project backlogs and recent activity among businesses in the construction sector and the architectural and design services sector. The Barometer points to mixed expectations for home renovation market activity in the first quarter of the year.

“Current Barometer readings and qualitative feedback reflect a mixed degree of caution about market conditions among contractors, architects and designers,” said Nino Sitchinava, Houzz principal economist. “It is notable that, relative to a year ago, expectations and recent activity among contractors are more subdued and project backlogs are considerably lighter. In contrast, the sentiments and backlogs of architects and designers are on par with a year ago, likely explained by a boost in new business activity in the last quarter of 2018. That said, businesses overwhelmingly cite rising costs of products and materials and customers’ reluctance to proceed with the projects due to these costs.”

In the construction sector, the indicator related to project inquiries and new projects decreased to 72 in Q1 (down seven points relative to Q4). The decline follows decreases in both components, with expectations for project inquiries falling to 72 in Q1 (down seven points), and expectations for new projects also decreasing to 72 (down seven points).

As far as expected business activity, the indicator related to project inquiries and new projects decreased to 72 in Q1 (down seven points relative to Q4). The decline follows decreases in both components, with expectations for project inquiries falling to 72 in Q1 (down seven points), and expectations for new projects also decreasing to 72 (down seven points).

The project backlog indicator slightly increased to 4.8 weeks nationally in Q1 (up 0.3 weeks relative to Q4). That said, overall backlog for the construction sector is 1.7 weeks below year-over-year levels.

The recent business activity indicator related to project inquiries and new projects decreased to 67 in Q4 (down four points relative to Q3). The decline follows a decrease in both project inquiry activity, which fell to 67 in Q4 (down six points), and recent new projects activity, which decreased to 66 (down three points).

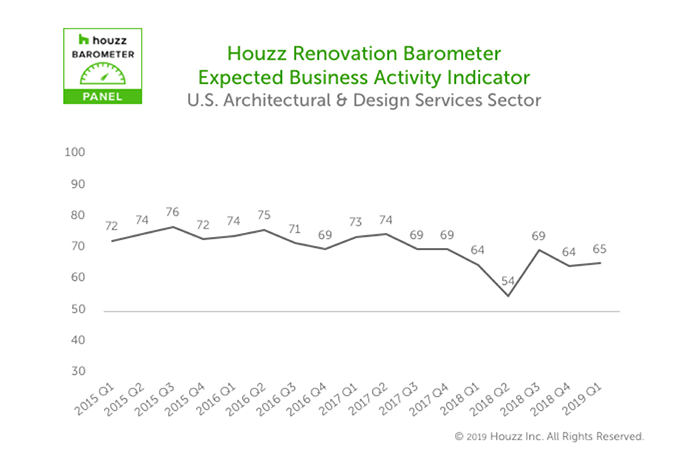

In the architectural and design services sector, the expected business activity indicator related to project inquiries and new projects remained nearly unchanged at 65 in Q1 (up one point relative to Q4). Expectations for project inquiries were at 64 (up one point) and expectations for new projects remained at 65.

The project backlog indicator slightly decreased to 4.7 weeks nationally in Q1 (down 0.4 weeks relative to Q4). The overall backlog for the architectural and design services sector is 0.2 weeks below year-over year levels.

In this in this sector, recent business activity indicator related to both project inquiries and new projects increased to 65 in Q4 (up five points relative to Q3). The uptick follows an increase in both recent project inquiry activity, which increased to 65 in Q4 (up three points), and recent new project activity, which increased to 65 (up seven points).

The recent business activity indicator related to both project inquiries and new projects increased to 65 in Q4 (up five points relative to Q3). The uptick follows an increase in both recent project inquiry activity, which increased to 65 in Q4 (up three points), and recent new project activity, which increased to 65 (up seven points).

More News

April 25, 2024 | Awards & Events

2024 Coverings Installation & Design Award Winners Announced

April 24, 2024 | People

Oatey Announces New COO and CCO

April 23, 2024 | Trends & Inspirations

Sustainability Report: More Education Needed for Green K&B Design

April 22, 2024 | Awards & Events, Trends & Inspirations

A Look Inside the 2024 Atlanta Homes & Lifestyles Southeastern Designer Showhouse

April 22, 2024 | KBB Collective

Top Designer Shares Favorite KBIS 2024 Products

April 2, 2024 | Sponsored

Whirlpool Corp. Brings Purposeful Innovation Home